Medicaid in New York gives health coverage to people with low income who meet certain rules. It covers doctor visits, hospital care, prescriptions, and more.

The 2026 rules are important because income limits and other details change each year with federal updates.

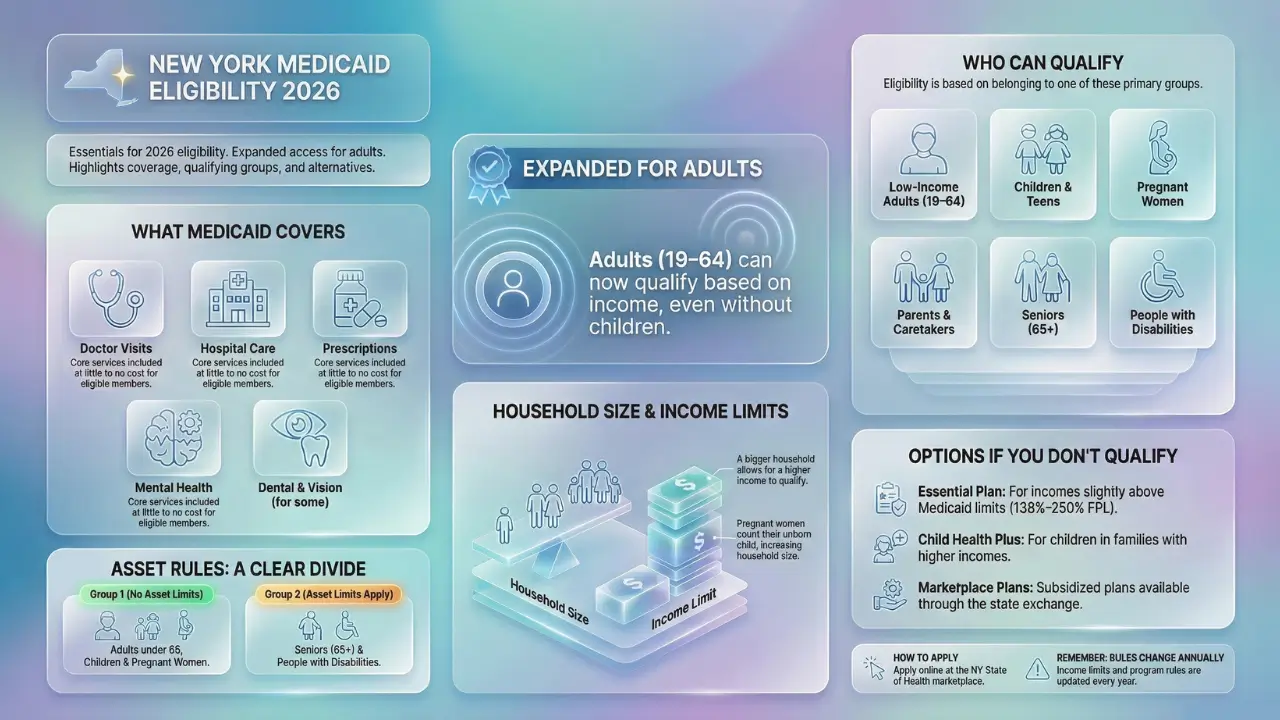

New York has expanded Medicaid, so more adults can qualify based on income alone. This sets it apart from states without expansion.

Eligibility rests on your group, such as being a child or a senior. It also factors in income, household size, and sometimes assets. Bigger households often have higher income caps.

Age matters too, with kids facing easier rules than some adults. New York aims to cover more people than many states. Still, not everyone qualifies.

Check your own case, as rules can differ. Coverage is not promised; you must apply and pass all checks.

Quick Eligibility Snapshot: New York Medicaid & Essential Plan (2026)

If you just want a fast answer, use this overview before diving into the details:

- Adults ages 19–64: Medicaid available up to 138% of the Federal Poverty Level (FPL)

- Children & pregnant women: Higher income limits apply

- Seniors age 65+: Income and asset limits apply

- Families: Larger households qualify with higher income limits

- Earn too much for Medicaid? The Essential Plan covers income up to 250% FPL

- Asset tests: Apply mainly to seniors and people with disabilities

This snapshot helps you quickly see where you may fit before reviewing full eligibility rules.

2026 Long-Term Care Income and Asset Limits

To qualify for Long-Term Care Medicaid in 2026, applicants must meet both income and asset limits. These limits are subject to annual adjustments and vary depending on marital status.

Income Limits (Single Applicant)

- Estimated monthly income limit: Under $1,800 per month

- Income includes sources such as Social Security, pensions, and retirement distributions.

- If income exceeds the limit, applicants may still qualify through planning tools such as a Qualified Income Trust (Miller Trust), depending on state rules.

Asset Limits (Single Applicant)

- Estimated asset limit: Up to $32,396

- This amount is confirmed for 2025 and expected to remain the same or adjust slightly for 2026.

- Countable assets generally include:

- Cash and bank accounts

- Investments

- Non-exempt real property

- Excluded (non-countable) assets typically include:

- One primary residence (subject to equity limits and residency rules)

- One vehicle

- Personal belongings and household items

Married Applicants (Spousal Protections)

- Married couples are allowed higher combined asset and income allowances.

- The spouse who is not applying (the “community spouse”) may retain:

- A larger share of assets

- A minimum monthly income allowance

- These protections are designed to prevent the non-applicant spouse from becoming impoverished.

Important Planning Considerations

- Medicaid enforces a 5-year look-back period on asset transfers.

- Gifts or transfers made during the look-back period can result in penalty periods and delayed eligibility.

- Advance planning is strongly recommended to protect assets while remaining compliant with Medicaid rules.

Note: All figures for 2026 are estimates until officially published by state Medicaid agencies. Limits and rules may vary by state.

What Is Medicaid in New York?

Medicaid is a program funded by the state and federal governments. It helps pay for health care for those who need it most. In New York, the Department of Health runs it.

The program serves over 7 million people. It covers a wide range of services, like check-ups, mental health care, dental, and vision for some.

New York Medicaid reaches children, pregnant women, families, adults, seniors, and people with disabilities. It offers broader coverage than in non-expansion states.

For example, low-income adults without kids can qualify. The goal is to keep people healthy and cut high medical costs.

If you get in, you pay little or nothing for care. New York also has managed care plans to organize your services.

Has New York Expanded Medicaid for 2026?

Yes, New York expanded Medicaid under the Affordable Care Act and keeps it for 2026. Expansion lets adults aged 19 to 64 qualify if their income is up to 138 percent of the federal poverty level.

This helps people without kids or disabilities who have low pay. Without expansion, many would lack coverage.

New York chose this to protect more residents. It covers over 2 million in the expansion group. If you earn too much for Medicaid, other plans may help.

Who Is Eligible for Medicaid in New York in 2026?

New York sorts people into groups for Medicaid. You must fit one and meet income rules for your household size. Here are the main ones:

- Low-income adults (ages 19-64): Thanks to expansion, you can qualify with income up to 138 percent of the federal poverty level. No need for kids or disability.

- Children: Kids under 19 qualify with higher income limits, often up to 154 percent for older ones. Babies can go higher.

- Pregnant women: Coverage goes up to 223 percent of the poverty level. It lasts through pregnancy and 12 months after birth.

- Parents and caretakers: Adults with kids under 19 can qualify if income is low, up to 138 percent for the family.

- Seniors (age 65+): They need low income, around 84 percent of the poverty level or less, plus asset checks.

- People with disabilities: Income and assets matter. Disability is checked by Social Security or state rules. Limits match seniors.

Rules differ by group. Most use MAGI, which looks at tax income. Seniors and the disabled use different counts.

You must live in New York and be a citizen or qualified immigrant. Apply even if unsure.

How Household Size Affects Medicaid Eligibility in New York

Household size counts the people you file taxes with, like you, your spouse, and dependents.

For Medicaid, it often means a tax filer plus kids under 19 or 21 if in school. Expectant mothers count the unborn child.

For adults and families, MAGI rules apply. This base size on your tax return. A single person has size one. Add a spouse and kids to raise it. A bigger size means a higher income limit.

For example, a family of four can earn more than a couple and still qualify.

For seniors or the disabled, size might differ, counting only those applying. Common mistakes include forgetting a dependent or adding non-family.

The wrong size can deny you. Use state tools to check. Report changes like a new baby right away.

Medicaid Income Limits in New York (2026)

Income limits depend on your group, household size, and federal poverty level. New York sets higher limits than non-expansion states due to expansion. Limits update each year.

For low-income adults, it’s 138 percent of the poverty level. Pregnant women reach 223 percent. Children go up to 154 percent or more based on age.

Parents match adult limits. Seniors and disabled have lower caps, around 84 percent, but can spend down extra income on bills.

Limits grow with household size. Use gross income from taxes, minus some deductions. Check the state chart for your group. Verify on official sites, as changes happen.

Medicaid Income Limits in New York (2026) for Seniors Age 65+

Seniors age 65 and older face different Medicaid rules than younger adults. Both income and assets are reviewed.

Estimated 2026 limits for a single senior:

- Income limit: Around 84% of the Federal Poverty Level

- Asset limit: Up to $32,396

- Countable assets: Cash, bank accounts, investments

- Exempt assets: Primary home, one vehicle, personal belongings

Seniors with income above the limit may still qualify using spend-down rules or long-term care planning strategies.

Asset Limits for New York Medicaid (Seniors and Disabled)

Asset rules hit seniors and people with disabilities most. These do not apply to kids, pregnant women, or expansion adults.

Countable assets include cash, stocks, and extra property. Exempt ones are your home, one car, and burial funds.

For community Medicaid, a single person can have up to $32,396. Couples get more. Long-term care like nursing homes matches this.

If over, spend down on care or exempt items. Married couples protect more for the healthy spouse. Get help to avoid mistakes.

Who Does NOT Qualify for Medicaid in New York?

Some miss out even with low income. If your earnings top the limit for your group and household, you are ineligible. For seniors or disabled, too many assets block you.

Non-residents of New York cannot join. Undocumented immigrants get only emergency care. False info on forms leads to denial. New York covers many, but rules are firm. If denied, appeal or try other plans. Do not assume coverage without checking.

Special Medicaid Programs in New York

New York offers extras beyond basic Medicaid. Managed Care plans handle your care through networks. Most enrollees use them.

Child Health Plus covers kids with family income too high for Medicaid, up to 400 percent of poverty. No cost or low premiums.

The Essential Plan helps adults from 138 to 250 percent of poverty with low-cost coverage.

Long-term care includes Managed Long-Term Care for home help. Waivers aid those with disabilities. These fill gaps for specific needs. Ask when you apply.

Medicaid vs Essential Plan in New York (2026): What’s the Difference?

Many New Yorkers confuse Medicaid with the Essential Plan. While both offer low-cost coverage, they serve different income groups.

| Feature | Medicaid | Essential Plan |

|---|---|---|

| Maximum Income | Up to 138% FPL (higher for kids & pregnant women) | Up to 250% FPL |

| Asset Limits | Yes (mainly seniors & disabled) | No |

| Monthly Premium | $0 | $0 |

| Age | All ages | Ages 19–64 only |

| Immigration Rules | Stricter | More flexible for some groups |

| Administered Through | NY State | NY State |

If you earn too much for Medicaid, the Essential Plan is usually the next best option.

Essential Plan Income Eligibility in New York (2026)

New York’s Essential Plan is a low-cost health insurance option for residents who earn too much for Medicaid but cannot afford private coverage. For the 2026 coverage year, eligibility is based on 2025 Federal Poverty Level (FPL) guidelines and administered through NY State of Health.

The plan continues to offer $0 monthly premiums for eligible individuals and families, making it one of the most affordable coverage options in the state.

2026 Essential Plan Income Limits (Up to 250% FPL)

Eligibility depends on household size and annual income.

| Household Size | Maximum Yearly Income | Monthly Income Limit |

|---|---|---|

| 1 | $39,125 | $3,261 |

| 2 | $52,875 | $4,407 |

| 3 | $66,625 | $5,553 |

| 4 | $80,375 | $6,698 |

| 5 | $94,125 | $7,844 |

| 6 | $107,875 | $8,990 |

Income limits are based on 250% of the Federal Poverty Level and apply statewide.

Essential Plan Eligibility Tiers

Your specific Essential Plan tier determines copays and cost-sharing:

- Essential Plan 200–250: Income between 200% and 250% FPL

- Essential Plan 1: Income between 150% and 200% FPL

- Essential Plan 2: Income between 138% and 150% FPL

- Essential Plans 3 & 4: For individuals ineligible for Medicaid due to immigration status

Key Requirements for the Essential Plan

To qualify in 2026, you must:

- Be 19–64 years old

- Live in New York State

- Not be eligible for Medicaid, Medicare, or affordable employer coverage

- Meet income limits based on household size

Children under 19 are covered separately through Child Health Plus.

Important 2026 Changes to Know

There is a proposed federal funding shift that may impact coverage:

- Essential Plan 200–250% FPL coverage is expected to end July 1, 2026

- Members in this income range may need to transition to Qualified Health Plans (QHPs)

- Essential Plan 1–4 are currently expected to remain unchanged

Affected members will receive advance notice and enrollment assistance.

How to Check Medicaid Eligibility in New York

Go to the NY State of Health website for a quick screener. Enter income, household, and group details. It shows if you might qualify.

Contact your local Department of Social Services office. Call 1-800-541-2831 for help. Bring proof like pay stubs. Checking saves time before applying.

How to Apply for Medicaid in New York

Apply online at nystateofhealth.ny.gov, it’s simple and fast. Or call 1-855-355-5777. In-person help comes from local social services offices.

Gather ID, income proof, household info, and immigration papers if needed. The state reviews in 45 days for most. Track online. If approved, choose a plan. Renew each year.

What to Do If You Are Not Eligible

Try the Essential Plan if income is a bit over, it has low costs. ACA Marketplace plans offer subsidies at healthcare.gov.

Local clinics give low-cost care. County programs help too. Reapply if income falls or family changes. Do not skip health needs.

Official Sources and References

This information is based on guidance from:

- New York State Department of Health

- NY State of Health Marketplace

- Federal Poverty Level (U.S. HHS)

- Centers for Medicare & Medicaid Services (CMS)

Eligibility rules and income limits are subject to change. Always verify details before applying.

Key Takeaways

New York’s Medicaid expansion in 2026 lets most adults ages 19–64 qualify based on income alone, even without children or disabilities. Eligibility depends on your group, such as child, pregnant woman, senior, or person with a disability. Household size affects income limits, with larger families allowed higher earnings, and pregnant women count unborn children. Income caps are higher than in many states, while asset limits apply only to seniors and people with disabilities. Those who do not qualify may still get coverage through programs like the Essential Plan or Child Health Plus. Rules and limits change yearly, so always check official sources before applying.